Fund performance

Past performance is not indicative of future performance

# inception date was 29 March 2011

Performance Summary

Fund Objective

The Trust aims to provide stable monthly income returns from a diversified portfolio of Asset-Backed Securities supplemented by a small allocation towards Short Term Money Market Securities.

The Trust will invest in Asset-Backed Securities and Short Term Money Market Securities which are normally only available to professional and institutional investors.

Our Investment Committee is pleased with the results of our fund, delivering on our objectives of capital stability and regular monthly income. We also maintain and manage liquidity closely across our fund should Unit Holders choose to redeem at any month end.

Fund Update

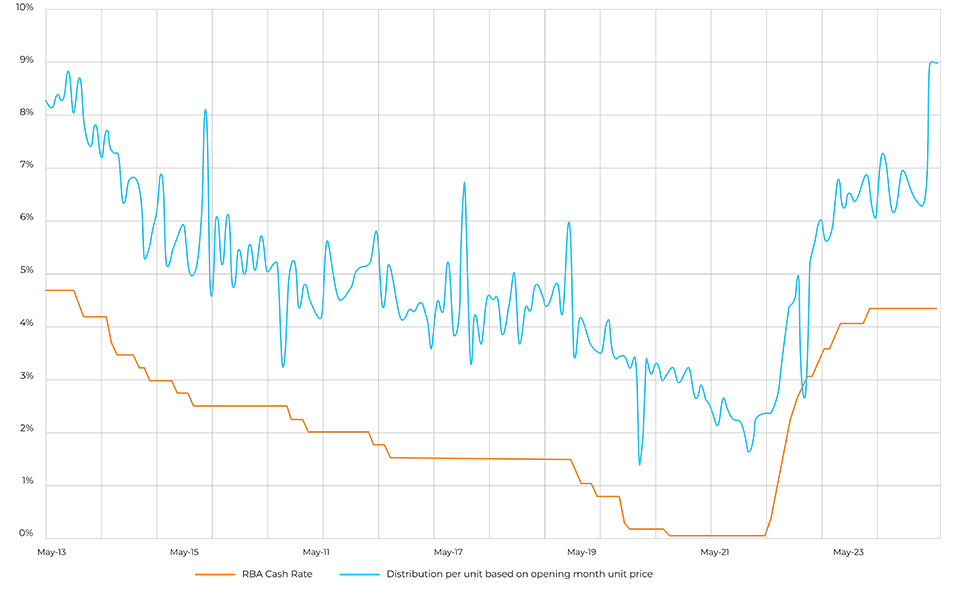

During May, the Fund Unit Price decreased slightly from 1.0584 to 1.0582. The Unit price has remained at elevated levels over the past year arising from continuing demand in credit markets for the underlying bond instruments in which our fund invests. The momentum is broad spread across most credit markets.

Unit Price volatility has remained low within a very narrow band. This is consistent with the fund objective of providing stable monthly income for our unit holders.

The fund has experienced low Unit Price volatility of an annualised 1% (calculated since August 2012). This means that the movement in Unit Price is quite narrow, tracking closely to the mean. This is consistent with a low risk managed fund.For the month of May 2024, our fund distributed an annualised 6.92%, representing a margin above the RBA cash rate of 2.57%.

The RBA has now lifted the cash rate target thirteen times for a total of 4.25%. This has resulted in a corresponding increase in the one month bank bill rate off which our fund investments reset above. The investments of the fund are all floating rate Notes which reset monthly. Hence, a rising cash rate will result in higher coupon receipts, increasing the distribution return of the fund. This means that increased collections, and therefore distributions, are anticipated in the future, continuing the trend illustrated in the above chart.

The RBA Cash rate and BBSW1m are 99.4% correlated over a ten year period. The RBA cash rate is widely understood and provides a useful explanation of fund returns, i.e. demonstrating that the fund returns are heavily influenced by changes in the RBA cash rate, as of course BBSW1m is highly correlated with the RBA cash rate.

Underlying asset quality remains strong, with low delinquencies across the underlying residential mortgages. We are pleased with our portfolio resilience however we do anticipate some increase in delinquencies associated with increasing mortgage rates. We expect all investments to be comfortably within tolerance over the months ahead.

The Total Return for the past 10 years was 4.45% per annum.

It is recommended that unitholders invest with a timeframe of 3-5 years. Over the past year three years, the Total Return was 4.45% per year, and over the past five years was 4.30% per annum.

The High Livez Fund is not capital guaranteed.

Australian Economic Update

Australian economic indicators released in May and early June showed the economy growing but at a soft pace. Real GDP rose in Q1 by only 0.1% q-o-q, 1.1% y-o-y. April retail sales rose 0.1% m-o-m, after falling 0.4% in March. Housing indicators were mixed-strength in April with home building approvals down 0.3% m-o-m, but the value of housing finance commitments up by 4.3% m-o-m. The labour market remained tight with employment up by 38,500 although a rising participation rate saw the unemployment rate lift to 4.1%. The Q1 wage price index showed annual wage growth edging down to 4.1% y-o-y from 4.2% in Q4 2023. The monthly CPI showed still sticky inflation in April with annual inflation lifting to 3.6% y-o-y, the second consecutive monthly increase. The RBA left the cash rate unchanged at 4.35% at its early May policy meeting although in subsequent commentary indicated that it would not hesitate to lift the cash rate if inflation stays sticky or rises.

Australian Credit Markets

Australian risk assets mirrored the sentiment seen in other global markets, with the Australian iTraxx moving six points tighter to 65 basis points. Physical credit assets performed well with issuance across Corporates, Bank senior and Tier 2 and Structured. Following the S&P announcement in April that moved the Major Bank’s Tier 2 rating from BBB+ to A-, secondary spreads have continued to react positively, moving tighter throughout the month. The strength of the Tier 2 market was demonstrated in the NAB 15NC5 $1.25bn transaction which had over $3.59b of interest. The deal was heavily oversubscribed and priced at +200 on 28th May. As of the 30th May the bond was trading at ~ +183 and has subsequently continued to move tighter. Despite continued primary issuance in structured markets being well supported, junior note pricing has moderated off the back of the markets strong rally throughout 2024.

Historical performance assumptions

*Total Return for the 10 years to 31 May 2024 and 5.39% since inception on 29 March 2011. The total return is the Fund’s consolidated performance over the period referenced. Performance is calculated on an initial investment of $10,000 with distributions reinvested. Ongoing fees and expenses have been applied however individual taxes are excluded. This website is prepared and issued by Firstmac Limited ACN 094 145 963 (Firstmac) the holder of Australian financial services licence (AFSL) number 290600 in respect of Firstmac High Livez ARSN 147 322 923 (Fund). Perpetual Trust Services Limited ACN 000 142 049, the holder of AFSL number 236648 is the responsible entity (RE) and the issuer of the units in the Fund (Units). A target market determination for the Fund is available at www.firstmac.com.au or by contacting Firstmac on 13 12 20. This website has been prepared without taking account of your objectives, financial situation or needs. Before investing in the Fund, you should consider whether an investment in the Fund is appropriate having regards to your objectives, financial situation and needs and obtain appropriate professional advice. Prior to making a decision about whether to acquire, hold or dispose of Units you should consider the product disclosure statement (PDS) for the Fund available at www.firstmac.com.au. Past performance is not a reliable indicator of future performance and may not be repeated. Restrictions may apply to the amount and timing of withdrawal requests – refer to the PDS for full details.

Welcome to firstmac.com.au _

Just in case we lose you, may I ask for your contact details....