Managed accounts vs managed funds

Learn more about High Livez

Despite this, they are still not well understood compared to managed funds, their big brothers that dominate the Australian investment scene.

Here we explain what managed accounts are, and what the differences are between these two popular vehicles.

What are managed accounts?

A managed account is an account that is owned by an investor, but managed by a financial adviser the investor has hired.

It typically contains financial assets such as shares, cash, or titles to property. The investment manager has been authorised to buy and sell assets without the client’s approval on each occasion, as long as they act in accordance with the objectives they have previously agreed with the client.

The manager is legally obliged to act in the best interest of the investor and will usually supply them with regular reports on the account's performance and holdings.

Crucially, the investor directly owns the underlying assets themselves, unlike a managed fund.

There are two main types of managed account.

- Separately Managed Accounts (SMAs) are usually governed by a constitution and a Product Disclosure Statement (PDS). SMAs are built on a 'model portfolio' basis by an investment professional. When the model portfolio changes, the investments in each account are rebalanced to reflect that.

- Individually Managed Account (IMA) –IMA are typically not registered with a PDS and offer greater personalisation than SMAs because they can be fully tailored to each client’s needs. IMA investors get a portfolio that has been created for them alone based on agreed investment strategies.

What are managed funds

When you invest in a managed fund, your money is put into a pool with other investors. Like a managed account, a fund manager then buys and sells assets, such as shares or bonds, on your behalf.

Unlike a managed account, you don't own the underlying investments directly. The fund owns them, and you own 'units' in the fund. The value of each unit in the fund will rise and fall with the value of the underlying assets held by the fund, and you can buy or sell more units over time. Most managed funds pay income or 'distributions' to investors.

One example of this type of investment is Firstmac’s High Livez managed fund, which recently celebrated its 10th anniversary.

High Livez invests in prime Residential Mortgage-Backed Securities, (RMBS), which are bonds secured against the mortgages of Australian home owners.

Firstmac aims to provide stable monthly income returns from these RMBS, and suits investors with a 3-5 year time horizon.

For more information please see here.

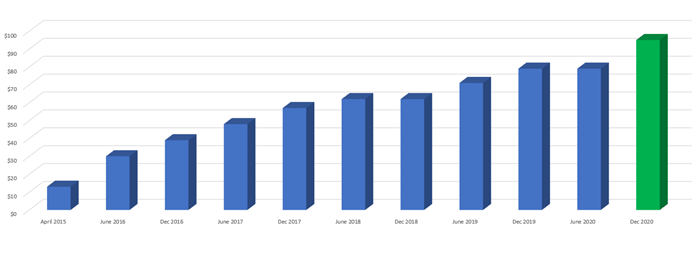

How big is the managed account market in Australia?

According to the Institute of Managed Account Professionals (IMAP), as at 31 Dec 2020, the managed account market in Australia ha $95.2 billion in funds under management. This was an increase of $15.49 billion in the 6 months from the 30 June 2020 FUM total of $79.71 billion.

The reported Net Funds Inflow from 30 June 2020 to 31 Dec 2020 was $6.97 billion.

Growth in Managed Accounts Funds under Management from 2015 to Dec 2020 ($ billions)

What is the difference between managed funds and managed accounts

Managed Account

- The individual investor owns the underlying investments such as shares or bonds.

- Investors receive all dividends, franking credits, and distributions directly.

- For equity-based strategies, the investor has beneficial ownership of the shares they are invested in, meaning they recieve company dividends and imputation credits that can improve tax outcomes.

- As the owner of the assets, the investor knows exactly what the account owns

Managed Fund

- The individual investor owns units in the fund.

- The fund receives all earnings and the fund manager income is distributed to investors in accordance with the PDS.

- The investor does not directly recieve company dividends or imputation credits.

- The investor owns a unit in the fund but doesn’t know what underlying assets the fund has or what transactions it has been involved in.

Pros and cons of managed accounts vs managed funds

Pros

-

Managed accounts can time purchases and sales of assets to reduce the investor’s tax burden, unlike managed funds which have many investors with different needs

-

The investor is informed about all transactions involving the assets in their managed accounts. Managed fund investors don’t own the fund’s assets, so they aren’t informed about each transaction

Cons

-

The minimum investment for most managed accounts is high, usually more than $100,000; while managed funds require a much lower amount, as little as $5000.

-

Investing or selling out of a managed accounts’ assets may take a significant amount of time; while shares in managed funds can often be bought or sold on a daily basis.

-

Annual fees, which have a big impact on overall investment returns, are typically much higher with managed accounts than managed funds.

So there you have it - two structures which both allow professional investors to manage investments on your behalf, but in quite different ways. As always, remember it is important to get independent financial advice before making any investment, to ensure it is suitable to your individual financial circumstances.